The impact of the policy of centralized land supply in 22 cities on real estate!

Policy of "centralized land supply in 22 cities"

According to recent media reports, the Ministry of Natural Resources issued a document on the classification and control of residential land, including four first-tier cities in the north, Guangzhou and Shenzhen, and 18 second-tier cities in Nanjing, Suzhou, Hangzhou, Xiamen, Fuzhou, Chongqing, Chengdu, Wuhan, Zhengzhou, Qingdao, Jinan, Hefei, Changsha, Shenyang, Ningbo, Changchun, Tianjin and Wuxi in 2021, and implemented two centralizations of residential land, i.e. centralized issuance of transfer announcements and centralized organization of land transfer. The above-mentioned urban residential land announcements shall not exceed three times. No unified time is set, for example, March, June and September in Tianjin, May, August and October in Jinan.

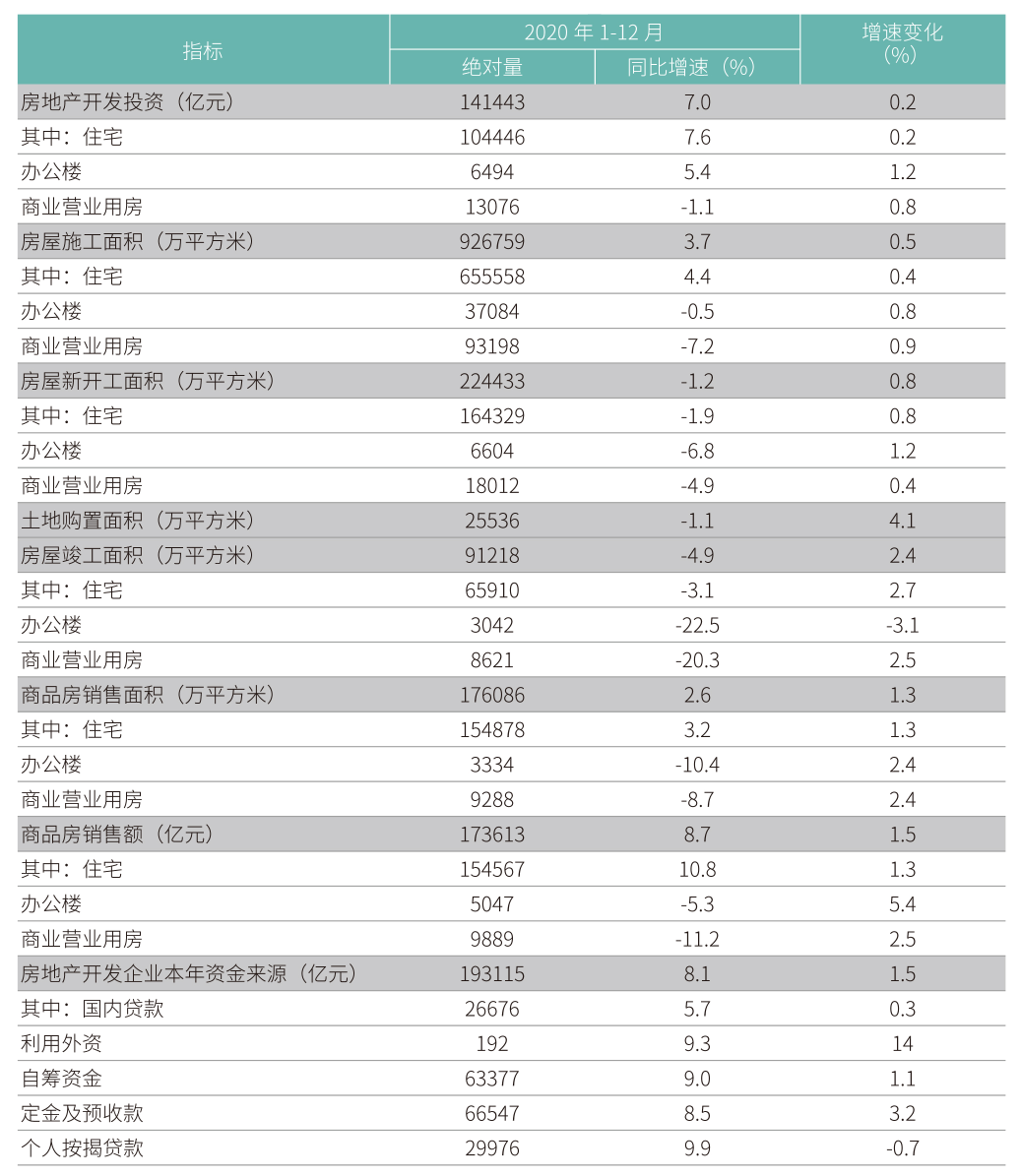

National real estate data in 2020

In 2020, the amount of investment in national real estate development was 14.1 trillion yuan, a year-on-year increase of 7.0%, down 2.9 percentage points over the previous year. The amount of investment in residential development from January to December was 10.4 trillion yuan, a year-on-year increase of 7.6%, up 0.2 percentage points over January to November, a decrease of 6.3 percentage points over the previous year, accounting for 73.8% of the total amount of investment in development.

In 2020, the sales area of commercial housing was 1.76 billion square meters, a year-on-year increase of 2.6%, down 0.1% over the previous year. From January to December, the sales area of residential buildings was 1.55 billion square meters, a year-on-year increase of 3.2%, the sales area of office buildings decreased by 10.4% year-on-year and that of commercial buildings decreased by 8.7% year-on-year.

In 2020, the sales volume of commercial housing was 17.4 trillion yuan, a year-on-year increase of 8.7%, up 2.2 percentage points over the previous year. From January to December, the sales volume of residential buildings was 15.5 trillion yuan, a year-on-year increase of 10.8%, the sales volume of office buildings decreased by 5.3% year-on-year, and the sales volume of commercial buildings decreased by 11.2% year-on-year.

△Data of national real estate development and operation in 2020

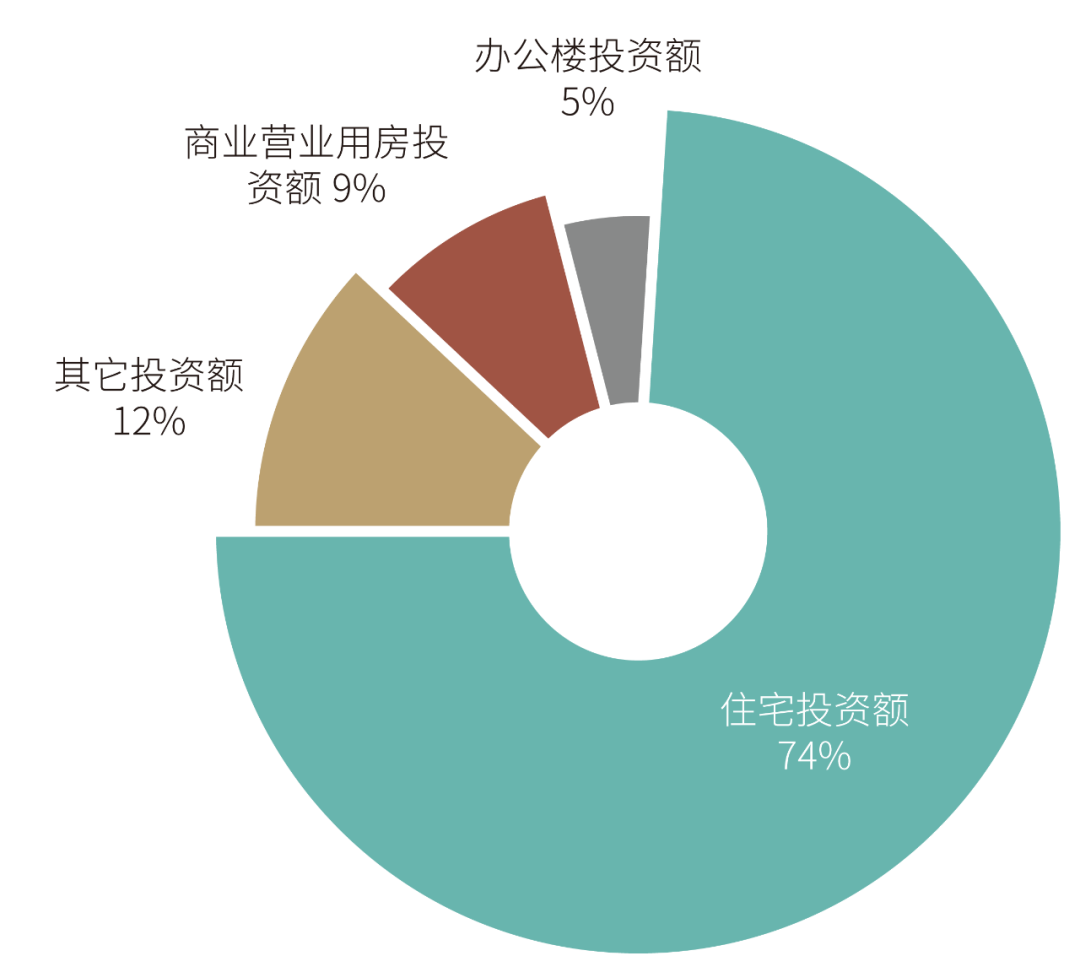

From the perspective of various types of business, housing is still the main component of real estate investment.

△ Proportion of real estate investment in various formats in 2020

Residential Land Supply Data of 22 Cities in 2020

According to CRIC data, the planned construction area of pure residential and commercial land supply in these 22 cities was 410 million square meters in 2020, accounting for 55% of the residential land supply area in 100 cities. The 22 cities that implement the policy of double centralization of land supply are also the first and second hot cities with high activity in the current land and real estate market.

△Land supply for pure residential and commercial projects in 2020 (data source: CRIC)

Equity sales data of 22 cities in TOP5 real estate enterprises in 2020

In 2020, the market concentration of real estate enterprises gradually increased, and the total sales of commercial housing of TOP5 real estate enterprises was 314.173 billion yuan, accounting for 18%.

△Equity sales of top five real estate enterprises in 22 cities in 2020 (data source: CRIC)

Concentration and differentiation

The real estate market is facing continuous regulation and control of policies, and the policy of centralized land supply helps to reduce vicious competition in the land market and promote the stability of land trading markets around the country, which is essentially an important manifestation of "stabilizing land prices, stabilizing house prices and stabilizing expectations". The policy of "centralized land supply" imposes certain restrictions from the perspective of local governments; the policy of "three red lines" directly restricts the financing of real estate enterprises, while the "centralized management system of real estate loans" restricts real estate-related loans from the perspective of financial institutions. From these three perspectives, we should comprehensively restrict the leverage of the whole industry, and ultimately hope to promote the steady and healthy development of the industry and reduce the systemic risk of the industry.

For hot cities, due to the development of regional economy and the net inflow of population, projects with better core regional plates can still attract a large number of enterprises and funds. The intention of participating enterprises is still high, the competition will still be very fierce, and the land price may remain at a high level. Housing enterprises have a tendency to concentrate on the core areas. Non-hot cities with relatively biased plates may face the trend of decrease in the number of participating enterprises and land prices under the policy of centralized supply.

Land market developed from 12 months of supply into centralized supply, land auction needs a lot of money, and housing enterprises are facing relatively strong financing constraints. In the short term, it may be difficult to have a large amount of funds to participate in competition of different cities and different plots, so the future housing enterprises will strengthen the project research and judgment work at the early stage, make selection in different regions and plots to achieve precise land acquisition. The number of enterprises and the scale of capital attracted by a single plot may decline, the whole land market will be more rational, and the differentiation between cities and plates will be further deepened.

Regulation policy for the whole real estate industry tends to normalization. The policy of "centralized land supply" not only tests the cash flow operation and financing ability of real estate enterprises, but also requires better cash flow matching ability. No matter for the leading real estate enterprises or small and medium-sized real estate enterprises, the current policy scenario is still lack of reference scenarios. Although the parties have analyzed the negative impact of policies on the development of small and medium-sized real estate enterprises, it is not excluded that some small and medium-sized housing enterprises focusing on deep development have better resource advantages in cities. Based on the understanding of the region, they can also bring opportunities for development.

The real estate development industry is a comprehensive industry integrating housing, municipal, industrial, construction and commercial development, which has a high degree of correlation and strong driving force, and has produced a huge "pulling effect". For real estate enterprises, the rhythm of land acquisition, construction and estate promotion is relatively stable, and the centralized land supply may bring relatively centralized estate promotion, which will also have a pulling effect on the upstream and downstream industry chain from material suppliers, construction companies and design companies.

Centralized land supply, centralized project development, future competition will also be reflected in the supply chain competition, and excellent supplier resources will in hot demand. Suppliers with core competitiveness will occupy a place, whether it is materials, total contract, design resources, etc. Scale, leading product and technology, leading service and support, first-class quality, and low total cost will be the criteria for supplier evaluation. For leading enterprises, the strong will remain strong and continue to accelerate growth, concentration will be further enhanced, different echelons of enterprises in the future business performance will continue to differentiate, and small and medium-sized companies continue to compete for market segments. 74% of the residential investment and centralized supply will continue to increase the market demand for the supply chain of the residential market. The supplier resources originally based on the public construction market will also invest resources in the residential market, and the residential market will also break out more independent supplier resources.

The improvement of supply chain concentration will also force enterprises to innovate and improve efficiency. Only by close cooperation with customers can we develop the overall competitive advantage of the supply chain.

Source of this article: National Bureau of Statistics, CRIC